The 2008 global financial crisis left deep scars on investor psychology, and many people have spent the past decade searching for signs that the next crisis is coming. While the risk of a crisis is never zero, we think investors are fighting the last war by focusing on financial crisis risks.

Following the outbreak of the coronavirus pandemic, the US Federal Reserve has adopted a no-holds-barred approach to supporting the financial system. This reflects lessons learned from 2008, as well as the fact that (unlike in 2008) the Fed isn't worried about bailing out irresponsible actors, as the current stress is due to an external event rather than excess risk-taking in the financial system. This has quelled financial panic and liquidity concerns.

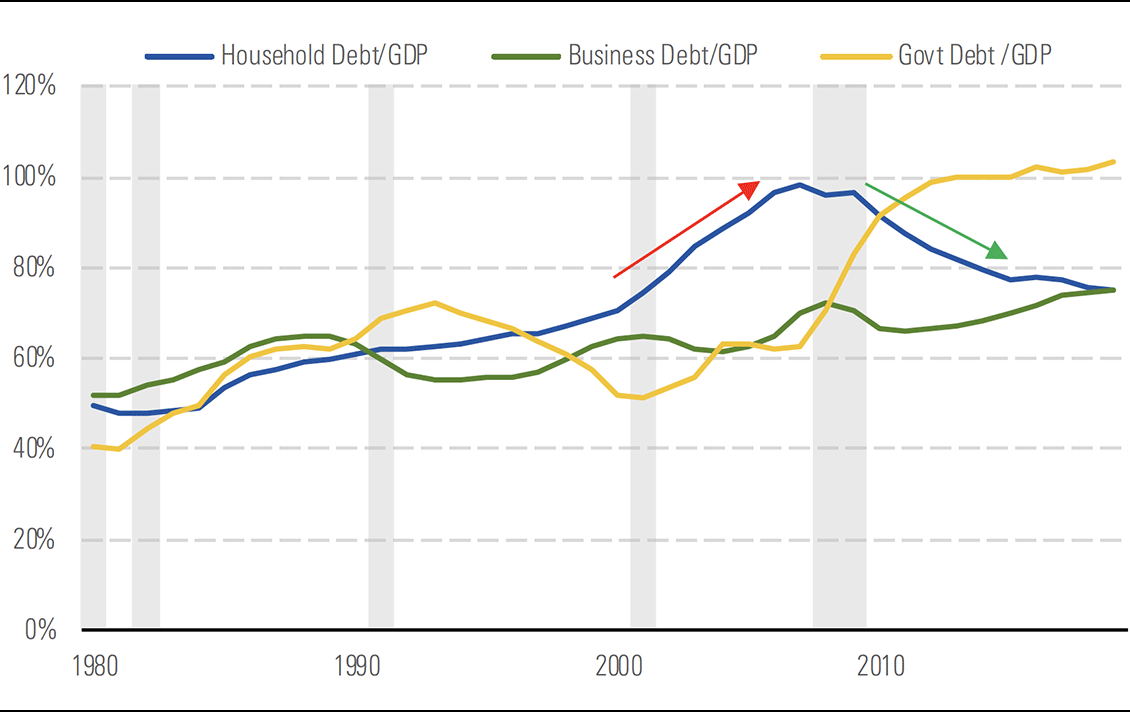

Meanwhile, the banking system is far better capitalised now, and any underlying vulnerabilities that could cause capital losses for the banks are far milder than prior to 2008. In particular, we see no boom in private borrowing akin to the household debt bubble of the 2000s (Exhibit 1).

Of course, a doomsday scenario in which the pandemic sinks the real economy could also bring down the financial system, but we think aggressive fiscal support and the eventual development of a vaccine will prevent this.

Exhibit 1. Current risks pale in comparison with household debt bubble in run-up to 2008

Source: The Fed, Morningstar

Key Takeaways

Avoiding a financial crisis remains a key pillar of our US economic thesis. In our research, we have examined the history of global recessions and found many of the worst recessions were accompanied by a financial crisis. We think the US will steer clear of a financial crisis during the Covid-19 recession. This is fundamental to our projection of just a 1% hit to long-run US GDP, far milder than the post-GFC impact to long-run GDP.

Unlike in 2008, moral hazard won't hamstring the Fed's support of the financial system. A key factor inhibiting central bank intervention in a typical financial crisis (such as 2008) is the moral hazard problem, or the fear that bailouts will reward bad behaviour and thereby corrode the long-term efficacy of the financial system. But the moral hazard problem is virtually non-existent in the case of the Covid-19 recession as the cause of financial stress is the pandemic, not bad behaviour in the financial system. This helps explain the Fed’s massive and unconstrained response to the crisis so far.

A liquidity crisis has been averted thanks to aggressive Fed intervention. The Office of Financial Research's financial stress index reached a near-term peak in March 2020 but still remained well below 2008 highs.

Financial system excesses going into this recession were much smaller than in the run-up to the 2008 crisis. Housing prices (a reliable measure of financial crisis risk) weren't overheated and overall private sector borrowing has diminished greatly since 2008, as the once spendthrift household sector has tightened its belt substantially.

US banks are far better capitalised than they were going into 2008. Key capital ratios have improved by 50 to 60% over the past decade. This capital should be ample to cover potential losses in the riskier parts of banks' balance sheets, such as leveraged loans or lending to sectors hard hit by Covid-19 like restaurants, tourism and, energy.

Government support is propping up private sector income. Personal disposable income is up substantially so far in 2020, as the impact of fiscal stimulus has more than offset the fall in pre-tax income. Even if no further stimulus is passed, we estimate that total US private sector after-tax income will be up about 9% in 2020 thanks to this boost. This will keep most private balance sheets in good shape, and help prevent a wave of defaults, which could destabilise the financial system.

Business sector debt build-up isn't a replay of the housing bubble. Much of the analysis on financial crisis risks has focused on the business sector, which has increased its debt to GDP to 75% at year-end 2019. This is far less severe than the household debt build-up during the housing bubble. Leverage in the non-corporate business sector is more elevated than in the corporate sector. However, thanks to falling interest rates, interest coverage ratios for non-corporate businesses are in good shape relative to their long-term history, despite the increase in leverage.