The ABC of finance says that to lower the overall risk of your portfolio you need to diversify your investments. This basically means having assets that move independently of each other.

Diversification is not limited to the division between equity and bond. Equity, for example, is a very broad asset class, made up of investments that are also quite different from each other. Sub-segments can be classified according to the market capitalisation of the company (large-cap, mid-cap, and small-cap), the reference market (developed countries or emerging markets), and the economic sector in which the company operates (industrial, financial, energy, and so on).

Diversification alone isn't enough. It is important to have an idea of how the various economic sectors represented by one’s equity exposure influence each other in order to avoid investing in instruments that are subject to very similar movements.

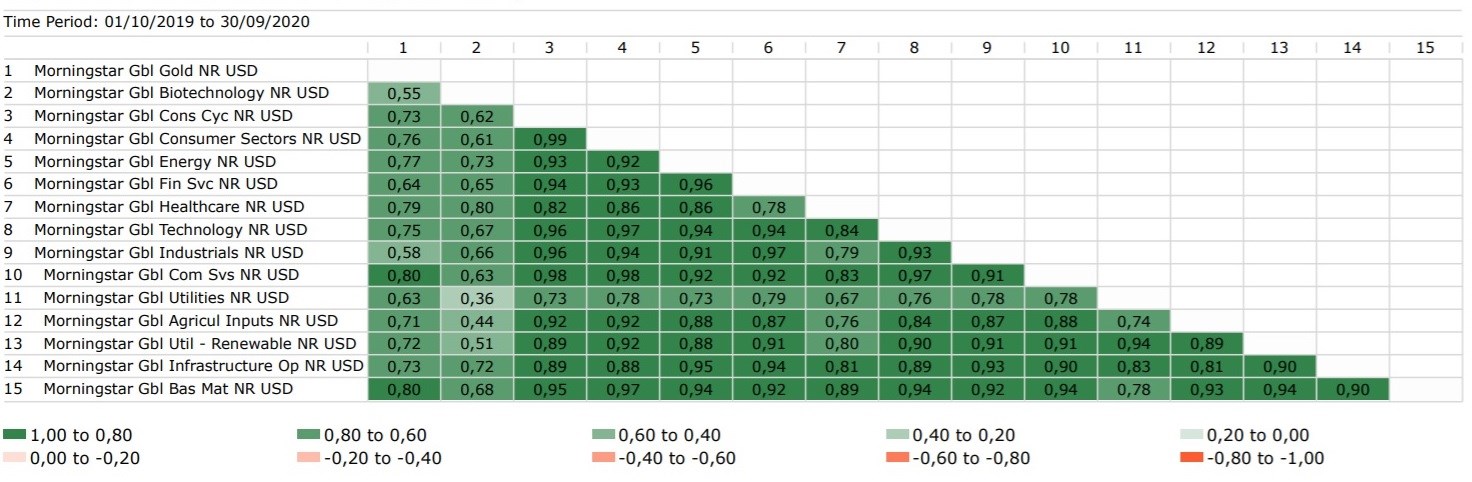

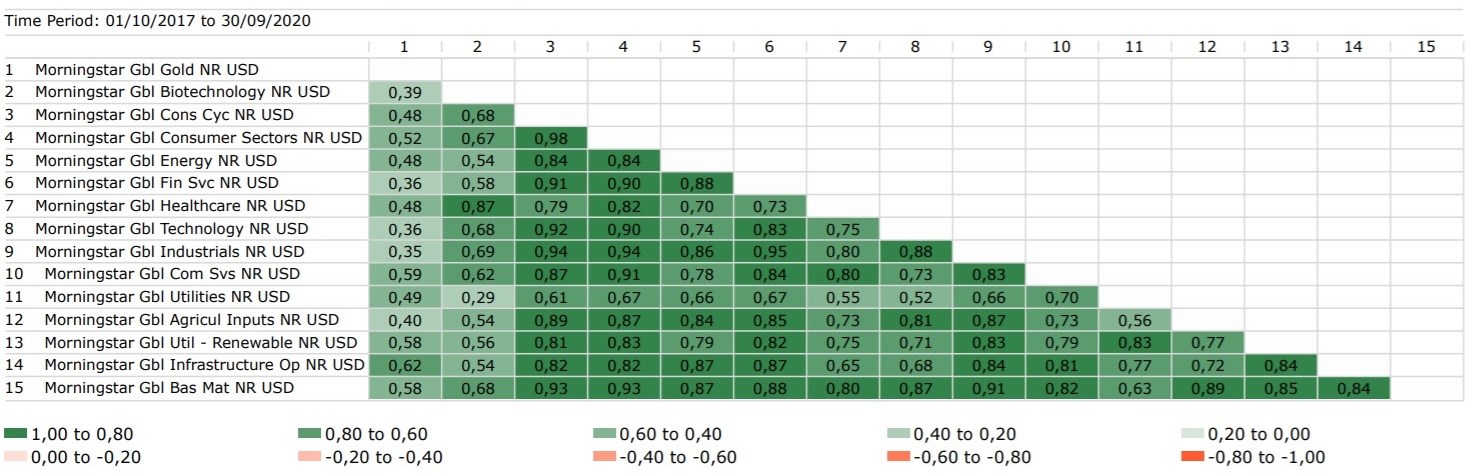

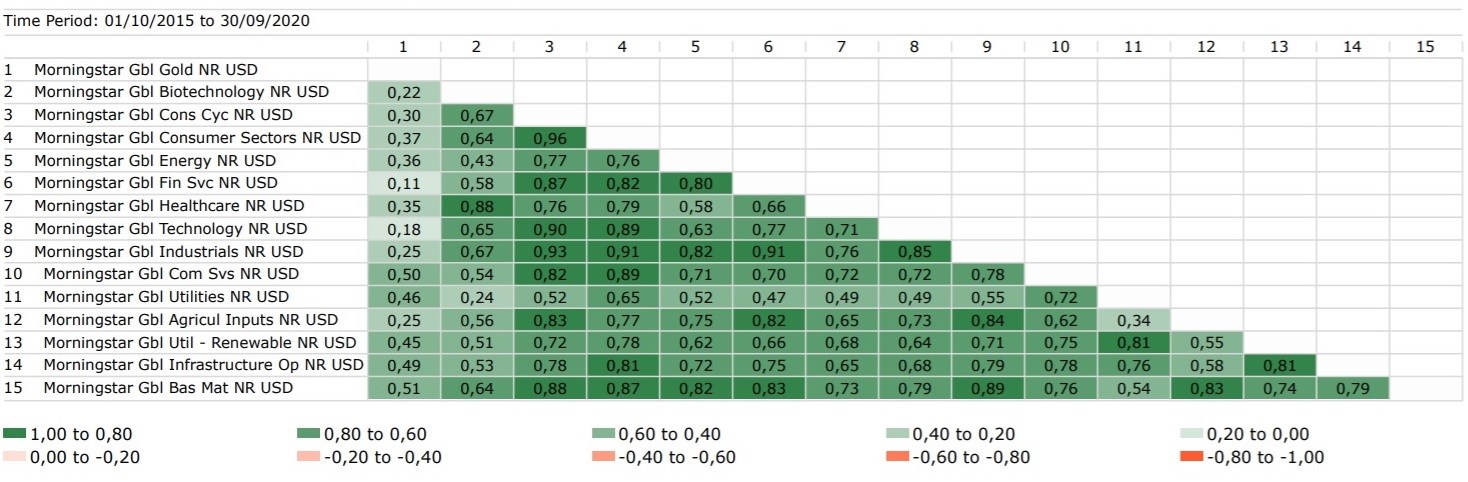

Looking at the underlying data, for example, we see that the correlation between the equity sectors has changed over the past five years. We see particularly that gold has lost the function of “diversifier” over the last 12 months that it has been historically famed for.

The correlation between the gold sector and the financial services sector, for example, jumped from 0.11 over five years to 0.64 over one year. That said, it should be noted that no negative correlations are found even at five years, a sign that this trend is not that recent.

Not surprisingly, the price of gold collapsed in March like all other asset classes, and then marked a strong rally between April and August, just like most international markets. In 2019, the yellow metal jumped 20% in a hugely positive year for global markets. In short, gold seems to have lost its function as a countercurrent investment.

According to Morningstar research, the basic materials sector, of which gold is an important part, is slightly overvalued currently (price/fair value of 1.02 as of Oct. 23, 2020; data in in U.S. dollars).

More generally, however, the market rally experienced last year and the crisis triggered by the pandemic this year, have actually increased the correlation coefficients between the various industries.

To interpret the tables below you can use the colors: the more the box tends to green, the higher the correlation is; on the other hand, the more the box tends to red, the more negative the coefficient is.

1 Year Sector Correlation

3 Year Sector Correlation

5 Year Sector Correlation

Source: Morningstar Direct. Data in euros as of Sept. 30, 2020.

The correlation coefficient measures how the performance of one instrument affects the performance of another: it varies between negative 1 and positive 1. A coefficient of 0 indicates that there is no correlation between the two funds. A coefficient of 1 indicates that there is a perfect positive correlation, which means that the two instruments move together: if one rises by 10%, the other does too, and vice versa. Obviously, in the case of perfect negative correlation (equal to negative 1) the ratio is inverse: if the first rises by 10%, the second loses 10%.