Companies poised to become industry leaders and those seeking to carve out wide Morningstar economic moats share some of the same qualities. For instance, they have a competitive edge – it could be high switching costs, powerful brands, or a significant cost advantage. In other words, they've begun to carve out an economic moat. But they aren't resting on their laurels. Instead, these companies continue to widen their moat by exploiting trends in their industries.

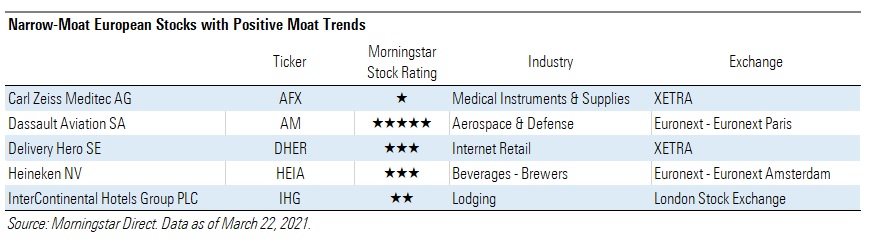

Our latest screen unearths European stocks with these qualities. We are looking at narrow-moat companies with positive moat trends - meaning their moats are strengthening. While there’s no guarantee these companies will eventually establish wide moats, they certainly have the right ingredients to do so. They’re strong stocks to buy at the right prices.

Perhaps not surprisingly, most of these well-run companies are fairly or overvalued according to our measures. But they’re all topnotch watchlist candidates.

A Closer Look at Three Names on the List.

Dassault Aviation SA

Dassault Aviation (AM) has an entrenched relationship with the French department of defence and is one of three global suppliers of large, long-range business jets. “We are positive on the medium-term prospects for Dassault underpinned by a solid defence order backlog, the potential to regain share in the business jet market, and the opportunity to grow support and service revenue”, says Joachim Kotze, equity analyst for Morningstar.

“Sales of Falcon business jets will suffer in the short term as a result of the coronavirus- induced economic headwinds. However, we believe Dassault Aviation is well-positioned to regain some of the lost market share with the launch of its Falcon model 6X aircraft in 2022.

"We estimate the group can achieve a 25% share of the 200-unit per year long-range market, translating to 50 units per year by 2024, up from 34 deliveries in 2020. Defense sales will be supported by a robust export order book with the remaining 40 Rafale fighter jets delivered over the medium term.”

Morningstar assigns a narrow moat rating to Dassault based on its intangible assets, which come as a result of the high level of engineering expertise required to develop complex military fighter jets and long-range business jets. With the support of the French government, Dassault successfully promoted the Rafale fighter jet to export markets and landed large orders with the Qatari, Egyptian and Indian armed forces from 2015 onward.

“Dassault is the leader of the next-generation European fighter jet project. The project is a consortium between France, Germany and Spain to replace the respective nations’ fighter jet fleet staring in 2035,” says Kotze.

Delivery Hero SE

British food delivery firm Deliveroo is seeking a valuation of up to £8.8 billion when it lists on the stock market in April, with a price range for its shares set at between £3.90 and £4.60.

“Although a well-capitalised Deliveroo isn't good news for competitors in the sector (including Just Eat Takeaway), we do see a path forward whereby both firms can profitably compete in some of those markets including the UK. This is based on the notion that if two platforms offer different restaurant listings (traditional takeaways for Just Eat, more premium end for Deliveroo), consumers would not think them as substitutes and thus it’s likely both platforms will survive”, says Morningstar’s equity analyst Ioannis Pontikis.

Delivery Hero is one of the fastest-growing food delivery operators in the world. It’s exposed to regions with attractive long-term structural characteristics and is well positioned to benefit from the secular trend of digitisation of food delivery orders. “Delivery Hero differs from other delivery operators in that its own-delivery business predominantly operates in countries with favorable characteristics, such as high population and restaurant densities, low/flexible minimum wages, relatively high average order values, and high frequency of delivery orders”, explains Pontikis.

With people spending more time at home, the pandemic has been a tailwind for takeaway platforms as penetration and usage have spiked to unprecedented levels and have remained elevated even during periods with no lockdowns or restrictions - an early sign of a sustained change in consumer behavior. Morningstar analysts expect the company to be able to support strong double-digit top-line growth as penetration and frequency of orders evolve. Read more on the Food Delivery sector in Morningstar's latest observer report.

Heineken NV

A favourite of veteran fund manager Nick Train, Heineken's new approach to long-term value creation focuses on four metrics: growth, profitability, capital efficiency, and sustainability and responsibility. Morningstar director of equity research Philip Gorham says:

“Growth targets are vague and non-committal, but we think Heineken (HEIA) has structural growth drivers that will allow it to generate above-average net revenue growth going forward. Volume growth in early stage markets such as central and southern Africa, premiumisation in its late stage developing markets such as Brazil, as well as a limited amount of pricing, should combine to drive mid-single-digit growth in the medium term. On profitability, Heineken plans to extract €2 billion, gross, in costs by 2023, primarily from reducing headcount by around 9%, at a cost of €900 million in operating and capital expenditure, and it targets an EBIT margin of 17% by 2023, which we think is achievable, and probably beatable.”

“Heineken’s returns on invested capital are structurally lower than those of AB InBev," says Gorham. “The ownership of pubs in the UK is an example of the heavy investments Heineken has made in its growth and competitive advantages. While it’s notable, and somewhat disappointing, that return on assets has been dropped as a performance metric in the green diamond strategy, we think if Heineken delivers on its volume growth and margin expansion opportunities, higher returns on capital should follow, and we anticipate mid-teens ROIC in the medium term, up from about 10% now on a normalised basis.”